Navigating the storm: What the regional crisis means for your Dubai property

Dubai insights

The Dubai rental market had every reason to expect a record year. January and February 2026 saw hotel occupancy running at 84.8%, short-term rental demand was strong, and investor confidence was high. Then, on 28 February 2026, the world’s attention turned to the Gulf and real estate markets shifted overnight.

What followed was one of the sharpest disruptions the UAE hospitality sector has seen since the pandemic, and a defining test of which property management models are built to survive it. For property owners and investors, the question is not whether this matters. It is what to do about it.

Amid the noise, owners and investors need clarity, not panic. This article covers what the data actually shows, which management approaches have held up, and why the right property management partner in Dubai makes all the difference when markets are at their most uncertain.

Executive summary

- Dubai hotel occupancy plummeted to 22.8% for the week of March 14 — the lowest since April 2020.

- Over 226,500 short-term rental bookings were cancelled across the UAE between February 28 and March 29.

- Holiday homes significantly outperformed hotels, with the STR segment projecting 50% occupancy for April and GuestReady on track for 60%.

- The active guest profile has shifted to domestic travellers, monthly-stay relocators, and essential corporate travel.

- A ceasefire announced April 7 and AED 1 billion in government incentives are driving early signs of recovery.

- Professional management — with dynamic pricing, multi-platform distribution, and flexible licence coverage — is the decisive advantage in this environment.

Part one

The shockwave: How the crisis hit Dubai’s hospitality market

What began as a strong start to 2026, with Dubai hotels recording 84.8% occupancy in January and February, was upended in an instant. On February 28, coordinated military strikes triggered immediate airspace closures across the UAE, Qatar, and much of the Gulf Cooperation Council.

The hospitality industry, which had been building toward another record year, was suddenly navigating its steepest decline since the darkest weeks of COVID-19.

| Dubai hotel occupancy, Jan–Feb 2026 (pre-crisis) | 84.8% |

| Dubai hotel occupancy, week of March 14 — lowest since April 2020 | 22.8% |

| UAE short-term rental bookings cancelled, Feb 28 – Mar 29 (AirDNA) | 226,500+ |

| UAE holiday home cancellation rate on Feb 28 vs. 14.5% monthly average (AirDNA) | 43.8% |

Sources: STR / CoStar (March 31, 2026); AirDNA / Short Term Rentalz (March 2026); World Property Journal; Business Today; CNBC.

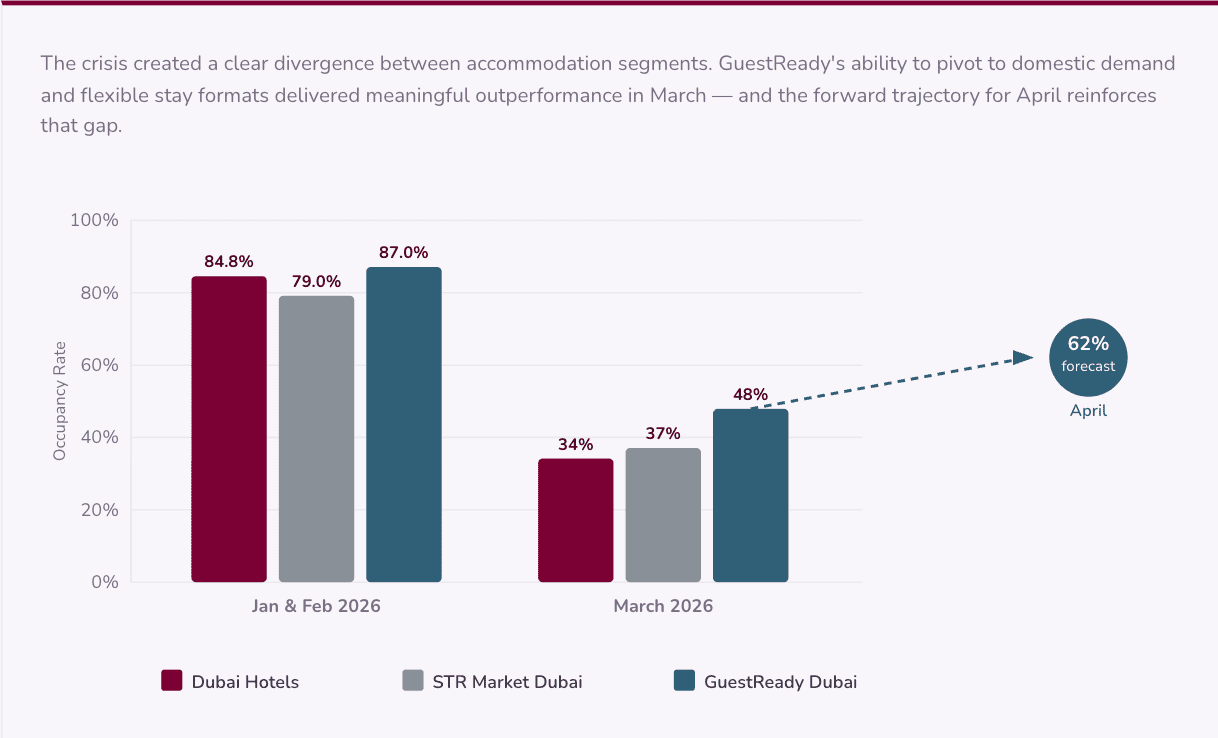

Monthly occupancy: Hotels vs. STR Market vs. GuestReady Dubai

| Hotels Jan–Feb: STR/CoStar (March 31, 2026). Hotels March: GuestReady estimate derived from CoStar weekly data (22.8% wk Mar 14; 28.2% wk Mar 21) — not a published monthly figure. STR Market: PriceLabs. GuestReady: internal booking data. April figure is GuestReady forward booking forecast only; no third-party hotel or STR market data available for April 2026 at time of publication. |

According to data published by STR and CoStar, Dubai’s hotel occupancy plummeted to 22.8% for the week ending March 14, the market’s worst performance since April 11, 2020. Five-star properties that had been running at 82% occupancy in January fell to below 35% within two weeks, with rack rates cut by 20 to 40% to chase a fraction of their normal demand.

Eid al-Fitr provided a brief reprieve, pushing weekend occupancy to 42%, driven almost entirely by domestic demand. But with international inbound travel severely suppressed and airspace operating on intermittent schedules, recovery was slow and deeply uneven.

The short-term rental sector absorbed an equally sharp blow. AirDNA data shows that on February 28 alone, the day the strikes began, UAE holiday rental cancellations hit 8,450 units, nearly three times the monthly daily average of around 3,100. The cancellation rate surged to 43.8% that night, compared with 14.5% for the rest of the month.

By March 29, more than 226,500 short-term rental bookings had been cancelled across the UAE since the conflict began. Over 80,000 short-stay reservations were lost in the first week alone, with the World Travel and Tourism Council estimating the Gulf region was losing $600 million in visitor spending every single day the conflict continued.

Regional divergence: not all markets are equal

Jeddah, backed by domestic and religious tourism and limited airspace disruption, held at 57% occupancy through Ramadan. Dubai bore the brunt, its deep integration with international travel becoming a vulnerability the moment those routes were severed.

More than 30,000 regional flights were cancelled between February 28 and mid-March, with EASA issuing an active advisory against UAE airspace operations.

Property markets reflected the same pressure. Transaction volumes fell roughly 25% in the first half of March, and residential prices slipped 4 to 5% from their February peak, while the DFM Real Estate Index dropped 20% in five sessions.

Analysts at CBRE called it “a temporary pause,” noting that most transactions were postponed rather than cancelled, leaving a substantial pipeline of deferred demand ready to return.

Part two

The new guest profile: How traveller behaviour has shifted

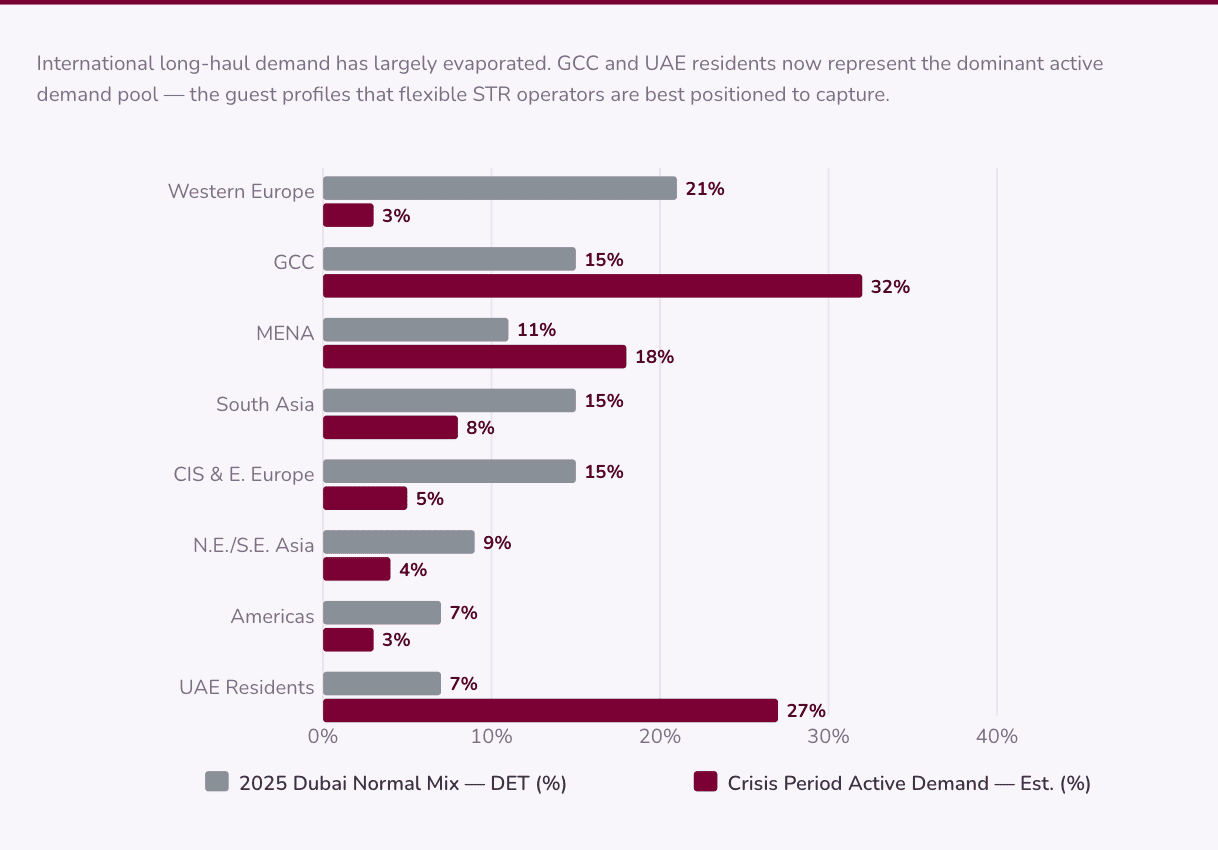

The guest profile active in Dubai today looks very different from January. International leisure travel has largely evaporated, with the Middle East tourism sector potentially losing 23 to 38 million visitors and $34 to $56 billion in revenue if tensions persist.

In their place: UAE residents seeking short breaks, relocating families needing temporary housing, corporate guests on essential travel, and remote workers extending their stays.

What unites them is a preference for privacy, flexibility, and self-contained space. Monthly stays have emerged as the dominant format, offering guests the flexibility of a short-term rental with the predictability of a longer commitment, and operators the income stability to weather the downturn.

“Demand didn’t completely disappear — it just shifted. People are actively looking for properties. They want deals. They want monthly stays. They want pet-friendly options.”

— Homevy, Dubai short-term rental operator, March 2026

Who is still travelling to Dubai? Demand source shift

| 2025 normal mix: Dubai Department of Economy and Tourism, full-year 2025 annual report. Crisis-period active demand: GuestReady estimate based on STR/CoStar airspace disruption data, WTTC regional travel suppression forecasts, and operator-reported booking profile shifts (March 2026). Crisis-period figures are estimates, not audited data. |

Part three

Hotels vs. Holiday Homes: The crisis puts the comparison in sharp relief

In ordinary times, hotels and holiday homes compete on broadly similar terms in Dubai’s premium accommodation market. In a crisis, their structural differences become starkly apparent, and they do not favour the hotel model.

| Dimension | Hotels | Holiday Homes |

|---|---|---|

| Pricing flexibility | Fixed rack rates, slow to adjust; aggressive discounting observed

Low flexibility |

Operators reprice daily; nightly rates and stay lengths adjustable in real time

High flexibility |

| Fixed cost structure | High fixed overheads (staffing, F&B, utilities) regardless of occupancy

High exposure |

Leaner operations; costs scale with bookings; easier to absorb a lean period

Lower fixed costs |

| Guest preference shift | Communal spaces, lobbies, shared lifts feel riskier to cautious travellers

Disadvantaged |

Private entry, self-contained units directly match current guest priorities

Structurally aligned |

| Demand diversification | Primarily leisure and corporate; heavily dependent on international arrivals

Concentrated risk |

Can pivot to domestic, monthly stays, relocators, essential corporate travel

Diversifiable |

| Recovery speed | Slow to rebuild demand; brand perception and distribution are slow-moving

Moderate |

Multi-platform listings reprice dynamically as demand returns

Faster recovery |

| Crisis impact | Dubai hotels: 22.8% occupancy week of March 14 — pandemic-era lows

Severely impacted |

Significantly impacted, but domestic and monthly demand provides a partial floor

Partially cushioned |

The disruption left no segment untouched, but the data tells an important story about relative resilience. While Dubai hotels hit 22.8% occupancy in the week of March 14 and five-star properties slashed rack rates by 20 to 40%, Dubai’s short-term rental market demonstrated a meaningful ability to absorb and adapt, buoyed by local GCC demand and traveller profiles who prefer the privacy and flexibility of an apartment over a hotel room.

The segment is projecting 50% occupancy for April, with GuestReady on track to reach 60% — a striking outperformance relative to the broader hospitality market during this period.

Operators who pivoted to monthly stays and domestic demand maintained a partial revenue floor that hotels, locked into their cost structures and distribution models, simply could not access.

Where hotels discounted defensively with little control over the outcome, holiday home operators made active choices about pricing, audience, and lease length. That flexibility is the silver lining, and it becomes the decisive advantage the moment recovery begins.

That said, tenants and guests across both short and long-term rentals are increasingly price sensitive, prioritising value and flexibility over commitment. This is making lease timelines less predictable and vacancy periods more likely, particularly for owners relying solely on traditional Ejari leases.

Well-positioned, competitively priced units continue to attract demand, but the advantage increasingly lies with Dubai holiday home investment strategies that can flex across rental formats.

Part four

What professional operators are doing to protect owner returns

The distinction between a poorly-managed holiday home during a crisis and a professionally-managed one is the difference between an empty calendar and a partly-filled one. The strategies being deployed by the best operators in this period are worth understanding.

01 — Aggressive dynamic repricing

Sophisticated operators are updating nightly rates daily, sometimes multiple times per day, based on live booking data, competitor pricing, and demand signals from booking platforms. This is not a race to the bottom but a calibrated response to market clearing prices that still maximise revenue per available night.

02 — Pivoting to monthly and extended stays

The three-to-six month stay format has become the dominant strategy: predictable income for owners, pricing that reflects current market conditions, and the flexibility to return to short-term nightly rates when international demand recovers. Relocators, corporate housing clients, and families in transition are actively seeking this format.

03 — Domestic and GCC-audience marketing

With international inbound travel suppressed, operators have reoriented marketing budgets toward UAE residents, Saudi, and wider GCC travellers who are still moving around the region. Staycation packages, family bundles, and “discover your own city” campaigns are filling gap periods.

04 — Multi-platform listing and distribution

Properties managed by professional operators are listed simultaneously across Airbnb, Booking.com, Vrbo, and regional platforms, with real-time inventory synchronisation. This maximises exposure to every available demand pool, something a self-managing owner simply cannot replicate manually.

05 — Regulatory positioning for recovery

Dubai’s recently enacted Law No. 4 of 2026, which regulates shared housing and short-term rentals, has provided institutional backing for the sector at exactly the right moment. Operators with properly licensed portfolios are positioned to recover cleanly when demand returns, without the legal uncertainty that unlicensed operators face.

Part five

Why GuestReady: The partner built for exactly this moment

In a rising market, property management competence is a nice-to-have. In a crisis, it is the difference between protecting your asset and watching it deteriorate. Not every operator among the best property management companies in Dubai is equipped to respond to a disruption of this scale. GuestReady is, and here is why that distinction matters for your property.

| In the Dubai market — through every cycle since 2018 | 8 years |

| Units managed across the UAE | 450+ |

| Guests hosted across our global portfolio | 1M+ |

| In revenue generated for property owners worldwide | $400M+ |

Unmatched flexibility — short, mid, and long term under one roof

Most holiday home operators are licensed for one thing: short-term stays. GuestReady holds both a a Real Estate business activity licence and Holiday Home Licence , which means we can manage your property under either the serviced apartment or Ejari model depending on what the market demands.

When international tourism is suppressed and monthly tenants are the active demand pool, we pivot without friction. When short-term visitors return, we pivot back. No change of operator required, no gap in income, no administrative disruption. This breadth of capability is rare in the Dubai market, and in the current environment it is one of the most valuable things we can offer an owner.

Extended reach to where demand actually lives right now

Beyond the global booking platforms, we have expanded your property’s presence to Blueground, Bayut, and Property Finder — the regional platforms where monthly and long-term tenants across the GCC are actively searching.

This is not a marginal addition. Whether you need Airbnb management in Dubai or longer-term tenant placement across GCC platforms, this is a direct pipeline to the exact guest profiles — relocating professionals, corporate housing clients, families in transition — who represent the primary source of accommodation demand during the current period.

A self-managing owner cannot easily access these channels or maintain verified, high-visibility listings across all of them simultaneously.

Full DET compliance — protecting you, always

Every property in GuestReady’s Dubai portfolio operates under a valid Department of Economy and Tourism Holiday Home Licence. This matters in any market, but it matters especially now, when regulatory scrutiny of the short-term rental sector is increasing and Dubai’s new Law No. 4 of 2026 has tightened the framework for shared housing and short-term rentals.

Owners with compliant, professionally managed properties are positioned to operate cleanly and recover quickly. Those without face fines of up to AED 200,000 and reputational risk at exactly the moment they can least afford it.

Eight years of Dubai market knowledge, applied today

GuestReady has been operating in Dubai since 2018. We managed through COVID-19, navigated the rebound of 2022, and have built our operational playbook through every market condition this city has produced. We are not improvising a response to the current crisis.

We are applying tested, refined approaches to a market we understand at a granular level: which locations hold demand longest, which guest profiles are still active, which pricing strategies protect yield without sacrificing occupancy. That institutional knowledge is not something you can replicate by reading market reports.

One partner, every owner profile, every situation

GuestReady owners do not fit a single profile, and neither do their circumstances. Some have lost a long-term tenant and need to activate their property quickly. Some manage their asset from overseas and need a trusted local operator to handle everything on the ground. Some are facing cash flow pressure and need income to resume as soon as possible.

Whatever your situation, we have the infrastructure, the licences, and the local presence to support you: from furnishing and listing your property to handling day-to-day operations, conducting viewings, and generating demand across every available channel.

You do not need to navigate these extraordinary circumstances alone or from a distance. We take care of everything, so your property continues to perform, wherever you may be.

The case, plainly stated

A self-managing owner faces this crisis with a single property, limited channel access, and no proprietary market data. A GuestReady owner faces it backed by a team of 300+ professionals, a portfolio of 4,000+ units globally, and eight years of local expertise. In uncertain times, that difference is not marginal. It is the margin.

The outlook: From crisis to recovery — and why the window matters now

The picture as of early April 2026 is meaningfully different from mid-March. On April 7, President Trump announced a two-week ceasefire with Iran.

Oil prices dropped over 13%, global equities rallied, and Dubai’s property and hospitality sectors registered the first signs of returning confidence. Understanding what comes next and positioning ahead of it is the most consequential decision owners face right now.

Dubai’s government response: AED 1 billion in direct market support

On March 30, Sheikh Hamdan bin Mohammed approved AED 1 billion (approximately US$272 million) in economic incentives running from April through September 2026.

The package includes a 100% postponement of the Tourism Dirham for three months and fee relief across hotels, hotel apartments, and holiday homes, a direct, funded commitment to accelerating the sector’s recovery.

Apr–May 2026

Early recovery — ceasefire unlocks pent-up demand

STR operators report an early uptick in domestic bookings. The EASA airspace advisory, under review as of April 10, is the key near-term trigger: if lifted, European carriers are expected to resume Gulf routes rapidly.

UAE travel agents expect traveller confidence to return to pre-war levels within two to three months if the ceasefire holds, with delayed April and May school holiday plans providing an immediate boost.

Q3 2026

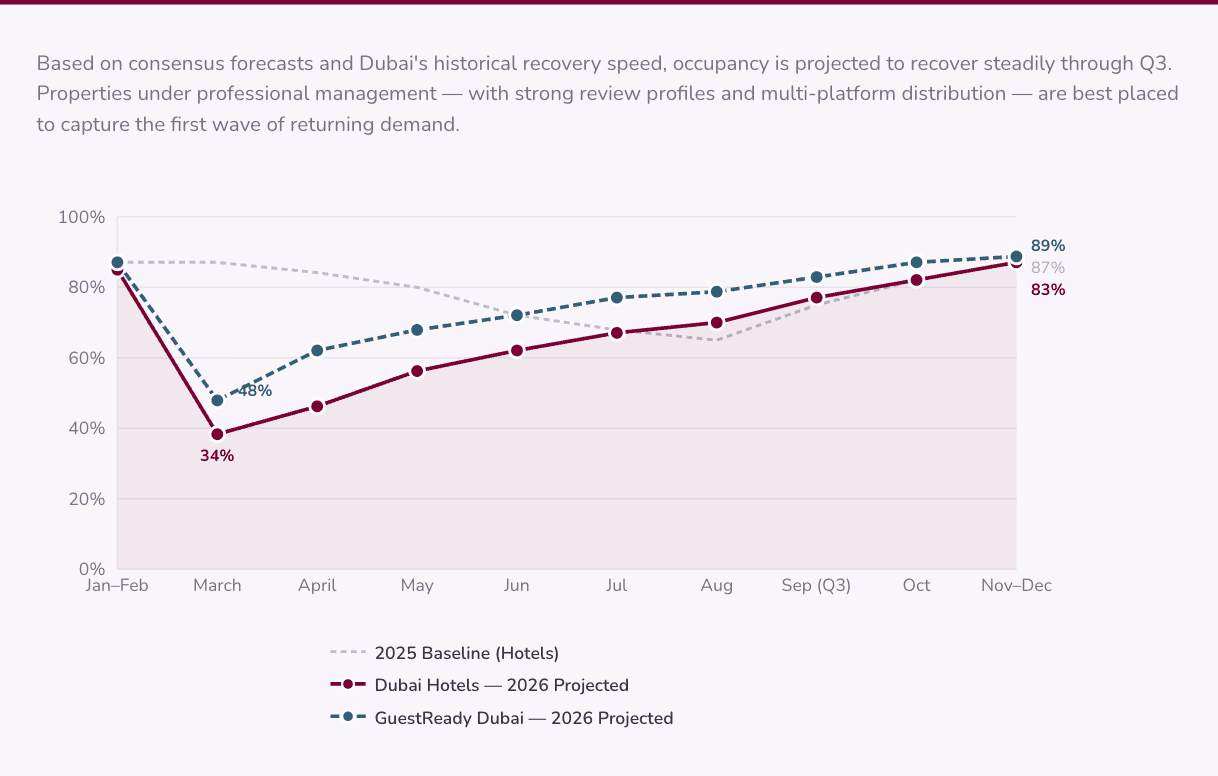

Demand inflection — the recovery wave arrives

Dubai has consistently rebounded faster than comparable markets after disruption. The 2003 Iraq war saw tourism recover within one quarter; the post-pandemic return was among the world’s fastest. The pipeline of over 226,500 cancelled STR reservations represents concentrated demand ready to return.

Properties under professional management with strong reviews will capture the first wave. Industry forecasters project 70 to 80% tourism recovery by October if the ceasefire holds.

Q4 2026–2027+

Structural growth resumes — Dubai’s trajectory intact

Dubai’s D33 agenda targets 33 million annual visitors. Population is expected to exceed 4 million. Holiday home yields of 8 to 12% for well-located, professionally managed units remain among the best risk-adjusted returns in global real estate. The crisis is a chapter. Dubai’s structural story is not.

What this means practically is straightforward: the reviews being written today, by the domestic guests, the monthly-stay relocators, the essential-travel corporate clients, will be read by the international leisure traveller who returns in Q3.

The investment in maintaining service quality during the lean period is not a cost. It is the most direct investment you can make in the rate and occupancy you command when the market turns, and on current evidence, that turn is already beginning.

Dubai hospitality recovery trajectory — projected occupancy (2026)

| Hotel recovery projection: GuestReady analysis based on STR/CoStar weekly trend data, Oxford Economics regional arrival forecasts, and Dubai historical recovery patterns (post-2003, post-COVID). Industry forecasters project 70–80% tourism recovery by October 2026 if ceasefire holds (Skift, April 9, 2026; Khaleej Times, April 9, 2026). GuestReady projections based on internal forward booking data. All figures from April 2026 onwards are projections. |

| Sources: Wego Travel Blog (April 8, 2026); Gulf News (April 8, 2026); Khaleej Times (April 9, 2026); Sherwoods Property (April 8, 2026); Skift (April 9, 2026); Dubai Media Office |

Frequently asked questions

How has the geopolitical crisis affected Dubai’s short-term rental market?

- Over 226,500 short-term rental bookings were cancelled across the UAE between February 28 and March 29. On February 28 alone, cancellations hit 8,450 units — nearly three times the monthly daily average — with the cancellation rate surging to 43.8% that night versus 14.5% for the rest of the month. The short-term rental segment has nonetheless outperformed hotels, with domestic demand and monthly stays providing a partial floor.

Why have holiday homes outperformed hotels during this crisis?

- Holiday homes offer structural advantages that become decisive in a crisis: the ability to reprice daily, lower fixed overheads, self-contained units that match current guest preferences, and the flexibility to pivot to domestic and monthly-stay demand. Hotels, locked into high fixed costs and distribution models built around international arrivals, have had far less room to manoeuvre.

What is Dubai’s Law No. 4 of 2026 and how does it affect property owners?

- Law No. 4 of 2026 regulates shared housing and short-term rentals in Dubai. Owners without a valid Department of Economy and Tourism holiday home licence face fines of up to AED 200,000 and reputational risk. Properties under professional management with full DET compliance are positioned to operate cleanly and recover quickly when demand returns.

When is Dubai’s hospitality market expected to recover?

- Industry forecasters project 70 to 80% tourism recovery by October 2026 if the April 7 ceasefire holds. The EASA airspace advisory — under review as of April 10 — is the key near-term trigger. UAE travel agents expect traveller confidence to return to pre-war levels within two to three months if the ceasefire holds. Dubai has consistently rebounded faster than comparable markets after previous disruptions.

What does the AED 1 billion government incentive package cover?

- Approved on March 30 by Sheikh Hamdan bin Mohammed, the package runs from April through September 2026 and includes a 100% postponement of the Tourism Dirham for three months and fee relief across hotels, hotel apartments, and holiday homes — a direct, funded commitment to accelerating the sector’s recovery.

What makes GuestReady’s dual licence valuable for property owners?

- GuestReady holds both a Holiday Home licence and a Real Estate business activity licence. This means we can manage your property under either the serviced apartment or Ejari model depending on what the market demands — pivoting to monthly tenants when international tourism is suppressed, and back to short-term nightly rates when demand returns. No change of operator, no gap in income, no administrative disruption.

| All market data cited in this article is sourced from STR/CoStar, AirDNA, CBRE, ANAROCK, WTTC, Skift, Khaleej Times, Gulf News, The National, Wego Travel Blog, Dubai Media Office, and publicly available research as of April 10, 2026. This article is intended for informational purposes and does not constitute financial or investment advice. |

Your Property. Our Expertise. Every Market Condition.

Whether you own a single apartment or a portfolio of units, GuestReady’s full-service holiday home management ensures your asset is protected today and positioned to outperform when demand returns.

With eight years in the Dubai market, 450+ units under management across the UAE, and distribution across every major global and regional platform, we have the infrastructure, the licences, and the local presence to support you through this, and to capture the recovery when it arrives.